Grande Prairie housing market stats for January to June 2026 compared to 2025. Home sales, average and median prices, days on market, and active listings, explained by a local realtor.

Is the Grande Prairie Real Estate Market Up or Down in 2026?

Short answer: fewer homes are selling, sale prices came in higher than last year, and inventory has steadily increased since January.

We're halfway through 2026, so I pulled the numbers from our local MLS to see how the Grande Prairie housing market compares to the same stretch last year. Here's what the data from January 1 to June 30 actually shows, and what I think it means if you own a home here or are thinking about buying one.

Grande Prairie Home Sales: First Half of 2026 vs 2025

In the first six months of 2026, 738 homes sold across all residential property types in Grande Prairie. Over the same period in 2025, that number was 809. That's a drop of just under 9%.

Looking at single family detached homes only (no condos, duplexes, or half duplexes), 566 sold this year compared to 592 last year.

Sales Prices Came In Higher, But Read the Fine Print

Across all residential sales in Grande Prairie:

The average sales price was $400,333 in the first half of 2026, up from $383,776 in 2025. The median sales price was $399,900, up from $379,900 last year, an increase of just over 5%.

For single family detached homes, the average was $430,563 with a median of $425,000, compared to a $421,608 average and $420,000 median in 2025.

Here's the part most market updates gloss over: a higher average sales price doesn't automatically mean every home in Grande Prairie is worth more. When fewer homes sell and the mix shifts toward newer or larger properties, the average climbs even if individual home values stay flat. Given what's happening with inventory (more on that below), I'd be careful about reading these price numbers as proof that values are rising across the board.

Homes Are Selling Slightly Faster

The average days on market dropped to 31 in the first half of 2026 from 35 in 2025. Well-priced homes are still moving quickly. The key words there are "well-priced."

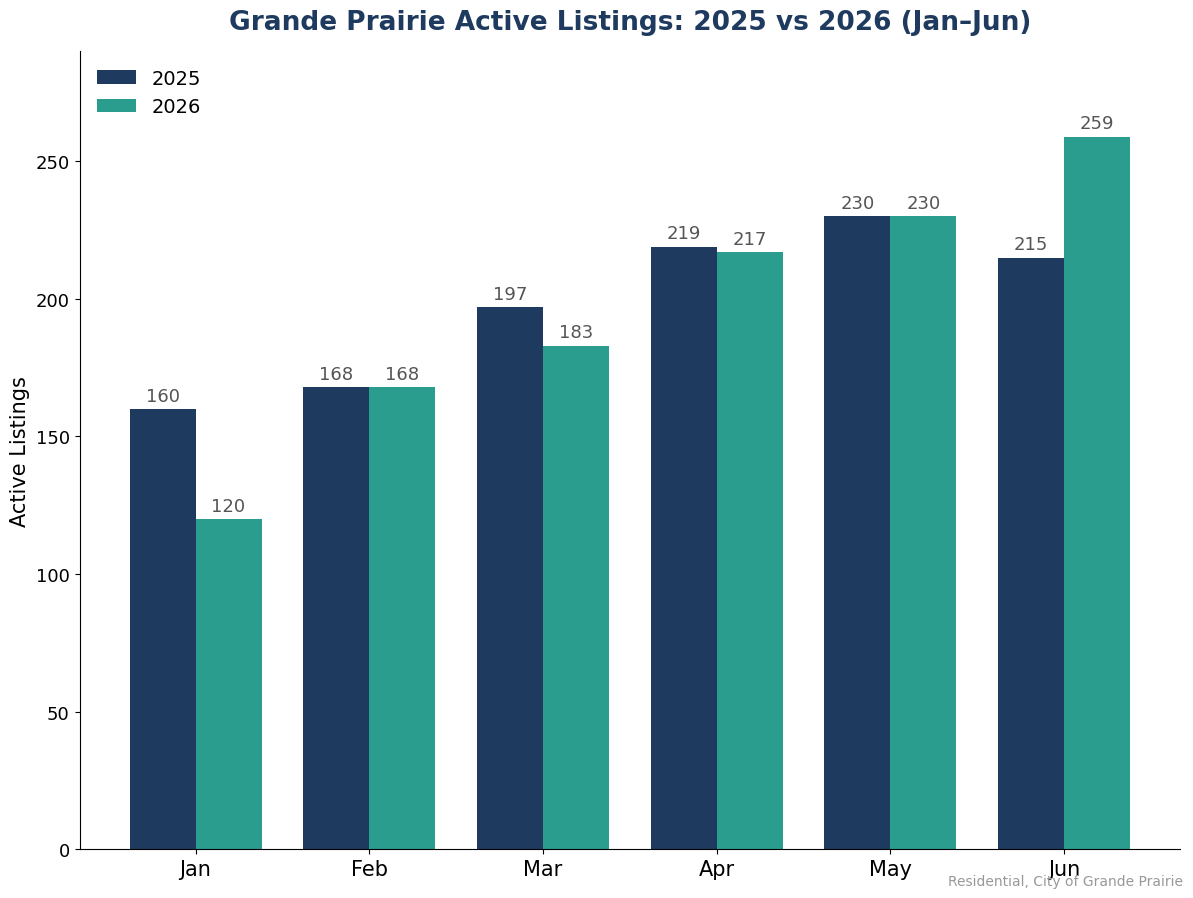

The Big Story: Inventory Has More Greatly Increased Since January

This is the number I'd pay the most attention to. Grande Prairie started 2026 with around 120 active residential listings. By the end of June, that number was roughly 260 (all residential, not just single family detached). That's more than double, and about 20% higher than June of last year.

For comparison, in 2025 inventory peaked in May at around 230 listings and then started pulling back. This year, it's still climbing heading into July. Although it has tapered off again, at the time of writing this.

What This Means If You're Selling in Grande Prairie

More listings means more competition. Buyers have noticeably more choice than they did a year ago, and homes that are overpriced will sit while the well-priced ones sell in days, sometimes hours. If you're planning to list this summer or fall, pricing accurately out of the gate matters more now than it has in a couple of years.

What This Means If You're Buying in Grande Prairie

This is the most selection Grande Prairie buyers have had in a while. With inventory still building and sales down from last year, you have more room to negotiate and less pressure to rush a decision. That said, the good homes at fair prices are still selling lightning fast, so being pre-approved and ready to act still matters. It does in any market.

Frequently Asked Questions

How many homes sold in Grande Prairie in the first half of 2026? 738 residential properties sold between January 1 and June 30, 2026, including 566 single family detached homes.

What is the average house price in Grande Prairie in 2026? The average residential sales price for the first half of 2026 was $400,333. For single family detached homes it was $430,563.

Is Grande Prairie a buyer's or seller's market right now? Grande Prairie is still very much a seller's market, but it's not the frenzied seller's market of the past couple years. Buyers have more options than they've had in years, which means pricing your home accurately matters now more than ever. Well-priced homes still sell fast.

How long does it take to sell a house in Grande Prairie? Homes averaged 31 days on market in the first half of 2026, four days faster than the same period in 2025.

Thinking about buying or selling in Grande Prairie? I'm happy to run the numbers for your specific home and neighbourhood. Reach out any time for a free, no-pressure home evaluation.

Data source: local MLS statistics, City of Grande Prairie residential sales, January 1 to June 30, 2025 and 2026.